Credit card debt in America is not just common — it’s normal.

According to Federal Reserve data, U.S. credit card balances regularly cross hundreds of billions of dollars. Many hardworking Americans carry balances at 18% to 29% APR, sometimes higher.

If you’re searching for how to pay off credit card debt fast, you’re not alone.

But here’s the truth most articles don’t tell you:

Paying off debt fast is not about motivation.

It’s about math + psychology + structure.

This guide will show you exactly how Americans are eliminating credit card debt strategically — not emotionally.

Save this article. You’ll refer back to it.

Why Credit Card Debt Becomes Dangerous So Fast

Before learning how to pay off credit card debt fast, you need to understand why it grows aggressively.

Most U.S. credit cards:

- Have variable APR

- Compound interest daily

- Charge late fees

- Penalize missed payments

Example:

You owe $8,000 at 24% APR.

Minimum payment: $200.

If you only pay minimum?

It can take years and cost thousands in interest.

That’s why paying minimum is not a strategy.

It’s a trap.

Step 1: Stop the Bleeding (Before You Start Paying Off)

This is where most Americans fail.

They try to pay off debt while still using the same credit cards.

If you truly want to pay off credit card debt quickly:

- Stop new spending on high-interest cards

- Remove saved cards from Amazon, Uber, food apps

- Use debit or cash for essentials

Psychology matters.

You cannot drain a bathtub if the tap is still running.

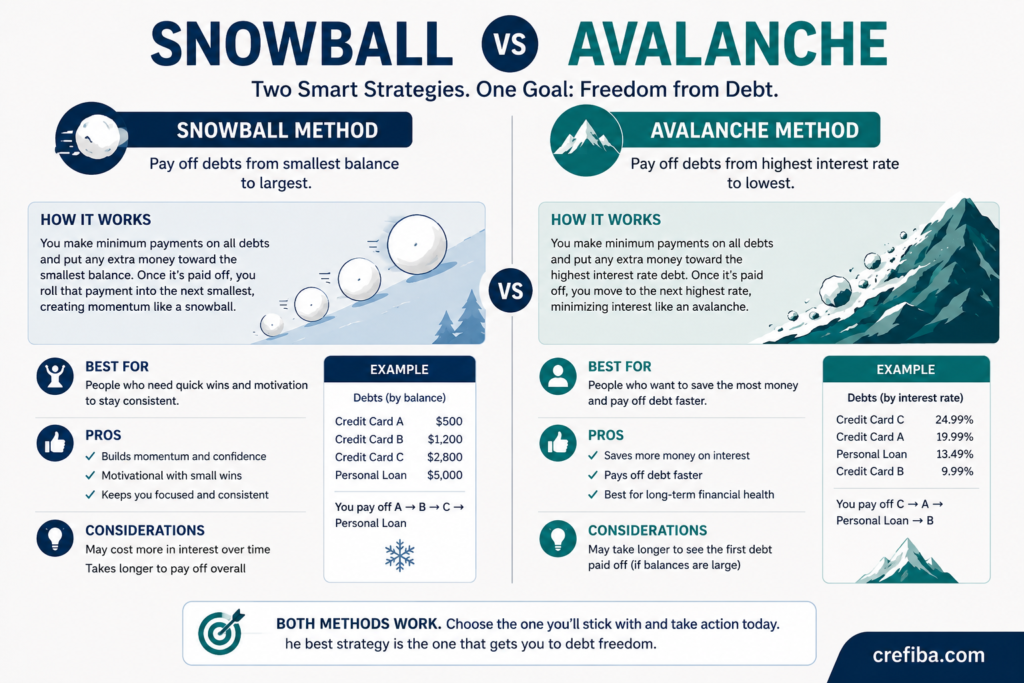

Step 2: Choose the Right Payoff Strategy (Snowball vs Avalanche)

This is the core of how to get out of credit card debt fast.

There are two proven methods.

1️⃣ Snowball Method (Behavioral Win Strategy)

You:

- Pay minimum on all cards

- Attack the smallest balance first

- Once paid off → roll payment to next smallest

Why it works:

Momentum.

When Americans see one card gone, motivation increases.

Best for:

- People needing emotional reinforcement

- Multiple small balances

Why Credit Card Debt Has Become a Serious U.S. Problem

Credit card debt in the United States is not just a personal issue — it’s a national financial trend.

According to Federal Reserve data, U.S. credit card balances have crossed $1 trillion, the highest in history. That means millions of Americans are carrying revolving balances month after month — often at APRs above 20%.

This is not about irresponsibility.

It’s about:

- Inflation

- Medical bills

- Emergency expenses

- Income instability

- Lifestyle creep

After the 2008 financial crisis, many Americans became more cautious with credit. But during and after the pandemic, credit usage surged again as savings declined and living costs rose.

Understanding this context is important.

You’re not alone — and this problem is bigger than just one bill. Even the Fedral reserve shows the data of Household debt

The Psychology Behind Paying Off Credit Card Debt Fast (Why It Grows So Fast)

Credit cards are designed to feel painless.

When you swipe a card, your brain doesn’t register the pain of spending the same way it does with cash. Studies in behavioral economics show that digital payments reduce “spending friction.”

Then comes the minimum payment trap.

When your statement says:

Minimum Due: $65

Total Balance: $5,400

Your brain chooses the smaller number.

But here’s the truth:

If you only pay minimums on a $5,000 balance at 24% APR, it can take over 10 years to pay off — and cost thousands in interest.

Credit card companies profit from this behavior.

Understanding the psychology is the first real step toward breaking the cycle.

How Credit Card Companies Calculate Interest (What Most People Don’t Know)

Many Americans think interest is charged once per month.

That’s not accurate.

Most U.S. credit cards calculate interest daily using:

Average Daily Balance × Daily Periodic Rate × Number of Days

Example:

If your APR is 24%

Daily rate ≈ 0.065%

That means interest accumulates every single day you carry a balance.

So even waiting a few extra days to pay can cost more than you think.

This is why speed matters when paying off debt.

Real Example (U.S. Context)– $8,000 Debt Case Study

Let’s take a realistic American scenario:

Credit Card Balance: $8,000

APR: 22%

Minimum Payment: $200

If paying minimum only:

• Payoff time → 6–7 years

• Total interest paid → ~$6,000+

If paying $500 per month:

• Payoff time → ~18 months

• Interest paid → significantly reduced

Same debt.

Different strategy.

Huge difference in outcome.

This is why “how to pay off credit card debt fast” is not just about effort — it’s about method.

Why Waiting Makes It Worse (The Compounding Effect)

Interest compounds.

That means:

You pay interest on interest.

If you delay aggressively paying it down:

• Your utilization stays high

• Your credit score suffers

• Your borrowing power decreases

High utilization (above 30%) signals risk to lenders.

So debt affects:

- Your credit score

- Your future mortgage approval

- Auto loan rates

- Even insurance premiums in some states

Paying it off fast improves more than just your bank balance.

The Hidden Cost of Carrying Credit Card Debt

Beyond interest, debt creates:

• Financial stress

• Reduced savings

• Limited investment opportunity

• Mental fatigue

Many Americans delay investing because they’re stuck servicing high-interest debt.

And here’s the mathematical truth:

If your credit card APR is 22%,

and your investments earn 8%,

You are losing 14% by prioritizing investing before paying off high-interest debt.

Debt payoff is often the highest guaranteed return you can get.

2️⃣ Avalanche Method (Mathematical Win Strategy)

You:

- Pay minimum on all cards

- Attack highest APR first

Why it works:

You save the most money.

Best for:

- Large balances

- High interest rates

- Analytical mindset

Which Is Better?

If discipline is strong → Avalanche.

If motivation is low → Snowball.

Both work.

The wrong choice is doing nothing.

Real Example: $15,000 Credit Card Debt Scenario (U.S. Context)

Let’s simulate.

Card A: $5,000 @ 29%

Card B: $6,000 @ 24%

Card C: $4,000 @ 18%

If you use Avalanche:

You attack 29% first.

You save thousands long-term.

If you use Snowball:

You attack $4,000 first.

You feel progress faster.

Speed is determined by:

How much extra you throw monthly.

Minimum payments don’t create speed.

Extra payments do.

Step 3: Increase Payment Power Strategically

If you’re serious about paying off credit card debt fast, you must increase payment capacity.

Three U.S.-realistic approaches:

1️⃣ Temporary Lifestyle Compression (90-Day Sprint)

Cut:

- Streaming duplication

- Eating out

- Unused subscriptions

- Premium memberships

Redirect savings to debt.

This short-term intensity accelerates payoff dramatically.

2️⃣ Lump Sum Injection Strategy

Use:

- Tax refund

- Work bonus

- Side gig income

- Sold unused items

Even one $1,500 lump payment cuts months off payoff timeline.

3️⃣ Income Boost Model

Temporary:

- Freelancing

- Rideshare

- Weekend gig

- Overtime shifts

Debt freedom often requires temporary discomfort.

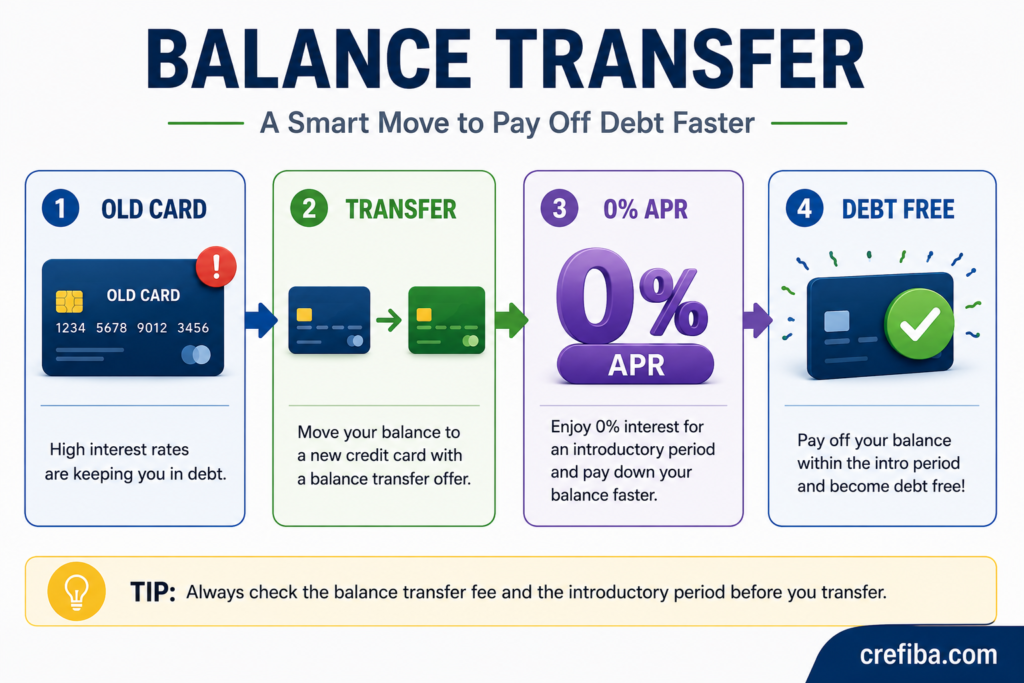

Step 4: Consider Balance Transfer (Smartly)

Many Americans search:

“How to pay off credit card debt fast with balance transfer?”

Balance transfer cards offer:

0% APR for 12–21 months.

But this only works if:

- You stop new spending

- You pay aggressively during intro period

- You account for transfer fee (3–5%)

Otherwise?

You delay the problem.

Used properly, it can save thousands.

Step 5: Debt Consolidation Loan (When It Makes Sense)

A personal loan can:

- Combine multiple cards

- Offer lower fixed interest

- Provide structured payoff schedule

Works best if:

Your credit score is fair to good.

If your credit score isn’t improving despite payments, read:

Why Your Credit Score Isn’t Increasing (Even When You Pay on Time)

(This helps you understand utilization impact.)

Step 6: How Paying Off Credit Cards Affects Your Credit Score

Many fear:

“If I close cards, will my score drop?”

Short answer:

Paying off debt improves score long-term.

Why?

Credit score factors include:

- Payment history

- Credit utilization

- Length of history

- Credit mix

Reducing utilization below 30% (ideally under 10%) increases score.

If you’re curious whether extremely high scores are possible, read:

Is a 900 Credit Score Possible in the USA?

Advanced U.S. Debt Optimization Strategies

🧾 When Minimum Payments Are Not Enough

Many Americans believe paying slightly above the minimum is enough.

It isn’t.

Minimum payments are structured by issuers to:

- Extend repayment timeline

- Maximize interest income

- Keep balances revolving

On a $10,000 balance at 24% APR:

- Paying minimum could take 20+ years

- Total interest may exceed the original balance

The system is mathematically designed to keep you in debt.

The solution is not “try harder.”

It is strategy.

🔍 The Hidden Cost of High APR Credit Cards

As of 2026, average U.S. credit card APRs hover between 20%–29%.

At 29.99% APR:

- Every $1,000 balance costs ~$300 per year in interest.

- Compounding works against you.

- One late payment may trigger penalty APR (often 29.99%+).

This is why attacking high-interest debt first is mathematically superior.

💳 Should You Consider a Balance Transfer?

Balance transfers can work — but only in specific conditions.

When It Makes Sense:

- You qualify for 0% intro APR (12–21 months typical)

- You can pay off the balance within promo window

- Transfer fee (usually 3–5%) is less than projected interest

When It Does NOT:

- You continue spending on old cards

- You only transfer without behavior change

- Your credit score drops due to utilization spike

Balance transfer is a tool — not a solution.

🏦 Debt Consolidation Loans — Smart or Risky?

A personal loan with lower APR (e.g., 10–15%) can reduce total interest.

But it only works if:

- You close or stop using paid-off cards

- Your loan rate is meaningfully lower than card APR

- You avoid extending repayment too long

Extending a 2-year payoff into 5 years may lower monthly payment but increase total cost.

Lower payment ≠ lower debt.

📉 How Credit Score Improves During Payoff

Here’s what most people misunderstand:

Your score does NOT jump immediately when debt is gone.

Improvement happens gradually through:

- Lower credit utilization

- On-time payments

- Reduced revolving balances

- Improved debt-to-income ratio

The biggest score boost often comes when utilization drops below:

- 50%

- 30%

- 10%

These are major FICO threshold zones.

🧮 Psychological vs Mathematical Payoff — What Actually Works?

Research shows:

- Avalanche saves more money.

- Snowball keeps more people consistent.

If you quit midway, math doesn’t matter.

The best method is the one you will follow for 12+ months without stopping.

Consistency > Perfection.

🚨 The Biggest Mistakes Americans Make While Paying Off Debt

- Paying only minimums

- Closing oldest credit card (hurts credit history)

- Missing one payment during payoff

- Using savings meant for emergencies

- Not building small emergency fund first ($1,000 buffer)

Debt freedom without safety net creates relapse risk.

🛑 When to Seek Professional Help

If:

- Debt exceeds 50% of annual income

- You’re missing payments monthly

- Collectors are calling

- APR exceeds 29% across multiple cards

Consider:

- Nonprofit credit counseling

- Debt management plans

- Hardship programs

Avoid for-profit “debt settlement” without deep research.

They may damage credit for years.

📊 Realistic Timeline: How Long Does It Actually Take?

If you pay:

- $200 extra per month → 2–5 years typical

- $500 extra per month → 1–3 years typical

- $1,000+ extra per month → under 18 months possible

Speed depends on:

- Total balance

- Average APR

- Income discipline

There is no overnight solution.

But there is a structured path.

The 90-Day Strategic Payoff Plan

If you want real acceleration:

Month 1:

- Stop new charges

- Choose strategy

- Set auto minimum payments

Month 2:

- Add lump payment

- Track progress weekly

Month 3:

- Increase attack amount by 10–20%

- Eliminate first card

Momentum begins here.

Mistakes That Slow Down Debt Payoff

- Only paying minimum

- Closing all cards immediately

- Taking new loans without discipline

- Ignoring APR differences

- Not building emergency buffer

You need at least small emergency savings.

Otherwise you fall back into debt.

How Long Does It Really Take?

Depends on:

Debt: $10,000

Extra Payment: $500/month

APR: 24%

Rough payoff:

About 2 years.

Increase payment to $800?

Cuts timeline significantly.

Speed is a math function.

Psychological Reality of Paying Off Credit Card Debt Fast

Debt creates:

- Anxiety

- Avoidance

- Shame

But structured payoff creates:

- Control

- Clarity

- Confidence

Financial freedom is not luck.

It’s systems.

Frequently Asked Questions (20 High-Intent U.S. Questions)

1. What is the fastest way to pay off credit card debt?

Aggressive payments using avalanche method combined with income boost.

2. Is snowball or avalanche better?

Avalanche saves money; snowball builds motivation.

3. Should I use a balance transfer?

Only if you commit to paying within intro period.

4. Does paying off credit cards improve credit score?

Yes, mainly through utilization reduction.

5. How much should I pay monthly?

As much above minimum as possible.

6. Is debt consolidation safe?

Safe if interest rate is lower and spending stops.

7. Should I close cards after paying?

Usually keep older cards open to preserve credit history.

8. What if I can’t afford extra payments?

Focus on income increase + expense trimming.

9. Does APR matter a lot?

Yes. Higher APR accelerates interest growth.

10. Can I negotiate interest rates?

Sometimes. Call issuer and ask for hardship program.

11. Is bankruptcy an option?

Last resort. Long-term credit damage.

12. How does utilization affect credit?

High balances lower score significantly.

13. Should I pay smallest or highest first?

Depends on behavioral vs mathematical preference.

14. How do late payments affect payoff?

They add fees and damage score severely.

15. Can side hustles help?

Yes. Temporary income spikes speed payoff.

16. Is 0% APR really free?

Only if paid before intro period ends.

17. How long does debt stay on report?

Accounts stay up to 10 years; negative marks up to 7.

18. What if I have multiple maxed cards?

Start with highest APR or smallest balance.

19. Can I use tax refund for payoff?

Yes — very effective strategy.

20. Is being debt-free realistic in one year?

Yes, if aggressive and disciplined.

Final Strategic Advice

If you truly want to know how to pay off credit card debt fast, understand this:

It’s not about hacks.

It’s about:

Structure

Discipline

Mathematics

Consistency

Thousands of Americans eliminate debt every year.

Not because they’re rich.

Because they’re strategic.

Start today.

Even one extra payment this month moves you forward.

The Crefiba Research Team creates easy-to-understand, accurate, and practical content on credit, personal finance, and banking in the United States. Our articles are carefully researched using trusted sources such as Experian, Equifax, TransUnion, and U.S. financial institutions, and are written to help everyday people make smarter financial decisions.

Learn more: About Crefiba • Editorial Standards