What is APR on a credit card?

If you use a credit card in the United States, APR is the single most important number determining how much your card actually costs you—yet it’s also one of the most misunderstood.

APR doesn’t matter when everything goes perfectly. It matters when life happens: a missed payment, a carried balance, an emergency expense, or a long billing cycle. This article explains APR clearly, slowly, and practically, using real U.S. credit card behavior—not theory.

This is a pillar guide written for Americans who want clarity, not marketing language.

What Is APR on a Credit Card? (Simple Explanation)

APR stands for Annual Percentage Rate.

On a U.S. credit card, APR is the yearly interest rate you’re charged if you don’t pay your full statement balance by the due date.

Here’s the simplest way to think about it:

- Pay your statement balance in full → APR usually doesn’t apply

- Carry any balance forward → APR starts charging interest daily

APR is not a fee.

APR is not a penalty (by default).

APR is the price of borrowing money from a U.S. credit card issuer.

According to the Consumer Financial Protection Bureau (CFPB), APR represents the annual cost of borrowing on a credit card and includes interest charges applied to unpaid balances.

How APR Works on U.S. Credit Cards (Step-by-Step)

APR on American credit cards is applied using daily interest, not yearly interest.

Step 1: APR is converted to a daily rate

Example:

- APR: 24.99%

- Daily rate ≈ 24.99% ÷ 365

Step 2: Interest accrues every day

If you carry a balance, interest is added each day, even on weekends.

Step 3: Interest compounds monthly

At the end of your billing cycle, all daily interest is added to your balance.

This system is used by Chase, Capital One, Citi, American Express, Discover, and nearly all U.S. issuers.

Why APR Exists on Credit Cards in the USA

In the U.S., credit cards are unsecured loans.

There’s no collateral. No asset backing your spending.

Because of that:

- Banks price in risk

- APR is higher than auto or home loans

- Federal law allows variable pricing

APR isn’t a trick—it’s a risk-management tool for lenders.

Types of APR on U.S. Credit Cards (You Must Know These)

Most Americans think they have “one APR.”

In reality, U.S. credit cards usually have multiple APRs.

Purchase APR

- Applies to normal spending

- Groceries, gas, online purchases

- Most commonly triggered APR

Cash Advance APR

- Much higher than purchase APR

- Starts immediately

- No grace period

Balance Transfer APR

- May be 0% temporarily

- Increases after promo ends

Penalty APR

- Triggered by repeated late payments

- Can exceed 29%

- Legal under U.S. law

Understanding which APR applies prevents surprises.

If high APR is causing your balances to grow faster than expected, focusing on the right habits becomes critical. Strategies like lowering utilization, timing payments correctly, and avoiding new debt can help—outlined step-by-step in our guide on 7 proven ways to improve your credit score fast.

Fixed APR vs Variable APR (U.S. Reality)

Almost all U.S. credit cards use variable APR.

That means:

- APR is tied to the prime rate

- When the Federal Reserve raises rates → your APR rises

- Issuers must notify you on statements

Fixed APRs are rare and usually temporary.

How the Federal Reserve Impacts Credit Card APR

When the Federal Reserve changes interest rates:

- Banks update the prime rate

- Credit card APRs adjust automatically

- Even old cards are affected

This is why Americans often notice APR increases without changing behavior.

Does APR Affect Your Credit Score?

APR does not directly affect your credit score.

However, APR affects:

- Monthly balances

- Utilization ratio

- Payment stress

Indirectly, high APR can lower your score if it leads to:

- Carrying balances

- Missing payments

- Increased utilization

While APR itself doesn’t directly change your credit score, high interest can make it harder to manage balances—which is one reason many people wonder whether extreme goals like a 900 credit score are even realistic. We break this myth down clearly in our detailed guide on is a 900 credit score possible in the USA.

Grace Period Explained (Where APR Doesn’t Apply)

Most U.S. credit cards offer a grace period:

- Usually 21–25 days

- Applies only if you paid the previous statement in full

Lose the grace period once → APR applies immediately on new purchases.

Why Many Americans Pay Interest Without Realizing It

Common reasons:

- Paying “minimum due”

- Paying current balance instead of statement balance

- Carrying small balances unintentionally

- Missing grace period rules

APR isn’t hidden—its mechanics are.

How to Avoid Paying APR on a Credit Card

The most reliable U.S. strategy:

- Pay statement balance in full

- Avoid cash advances

- Track billing cycle dates

- Use 0% APR offers responsibly

- Keep utilization under 30%

APR avoidance is about timing, not income.

Final Takeaway

APR isn’t evil.

APR isn’t a trick.

APR is simply the cost of borrowing in the U.S. credit system.

Once you understand how it works, you control it—not the other way around.

Frequently Asked Questions (FAQs)

1. What is a good APR on a credit card in the USA?

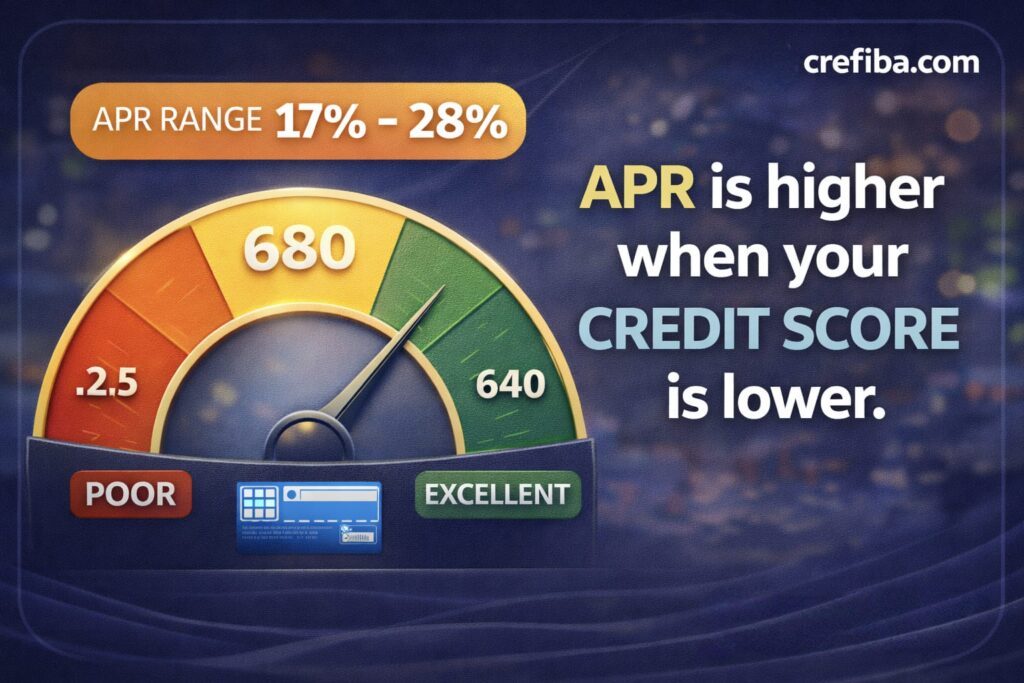

A “good” APR depends on your credit profile. Excellent credit holders may see APRs in the high teens, while average credit often means mid-to-high 20s. APRs below 20% are considered competitive in the U.S. market.

APR varies by issuer, card type, and economic conditions. There is no universal “best” APR—only better relative offers.

2. Why is credit card APR so high in the United States?

U.S. credit cards are unsecured and designed for short-term borrowing. Banks price APR higher to offset default risk and operational costs.

Federal law allows flexible APR pricing as long as disclosures are clear, which is why U.S. APRs are higher than many countries.

3. Does everyone get the same APR on the same card?

No. Most U.S. cards offer APR ranges. Your exact APR depends on your credit score, income, and history at approval time.

Two people can hold the same card with different APRs.

4. Can APR change after you’re approved?

Yes. Variable APRs change with the prime rate. Penalty APRs can also apply if payment rules are violated. Issuers must notify you of significant APR changes.

5. Is APR charged monthly or yearly?

APR is an annual rate, but interest is calculated daily and applied monthly.

This daily calculation is why balances grow faster than expected.

6. What happens if I only pay the minimum due?

You’ll avoid late fees, but APR will apply to the remaining balance. Interest accumulates daily. This is one of the most expensive ways to use a credit card.

7. Is 0% APR really interest-free?

Yes, during the promotional period. After it ends, standard APR applies to remaining balances. Missing one payment can cancel the promo early.

8. Does APR apply to new purchases immediately?

Only if you lost your grace period. Otherwise, APR applies after the due date.

Grace periods reset only after full balance payoff.

9. Is APR different for rewards cards?

Rewards cards often have higher APRs because benefits cost issuers money.

Rewards only make sense if you avoid interest.

10. Can APR be negotiated?

Sometimes. Long-term customers with good payment history may request reductions.

Results vary by issuer.

11. What is penalty APR?

A higher APR triggered by repeated late payments. It can apply for months or indefinitely. Penalty APRs are legal but must be disclosed.

12. Does APR matter if I pay in full?

No. APR doesn’t apply if you never carry a balance. Many disciplined users ignore APR entirely.

13. Why does my APR differ from my friend’s?

Credit profiles differ. Payment history, utilization, and income affect pricing.

APR is individualized risk pricing.

14. Is APR the same as interest rate?

APR includes interest but may reflect additional pricing elements.

On credit cards, APR and interest rate are often used interchangeably.

15. How do balance transfers affect APR?

Promotional balance transfers may have 0% APR temporarily, then revert to standard APR. Transfer fees still apply.

16. Does APR affect minimum payment?

Yes. Higher APR increases interest, which increases minimum payments over time.

This can trap balances longer.

17. Can APR go down when rates fall?

Yes, for variable APR cards tied to the prime rate. Reductions are usually slower than increases.

18. Is APR capped by law in the USA?

No federal cap exists. Some states regulate local issuers, but national banks often bypass caps. This is why APRs can exceed 29%.

19. What APR applies to fees?

Fees may accrue interest immediately, depending on issuer policy. Always read fee disclosures.

20. Should APR be my main factor when choosing a card?

Only if you plan to carry a balance. Otherwise, rewards, fees, and usability matter more.

APR matters when discipline breaks.

The Crefiba Research Team creates easy-to-understand, accurate, and practical content on credit, personal finance, and banking in the United States. Our articles are carefully researched using trusted sources such as Experian, Equifax, TransUnion, and U.S. financial institutions, and are written to help everyday people make smarter financial decisions.

Learn more: About Crefiba • Editorial Standards